Compound Interest, the 8th Wonder of the World

You’ve heard of the 7 wonders of the world; places like the Taj Mahal, the Roman Colosseum, and the Great Wall of China. But do you know what the 8th wonder is? According to Nobel Prize Winner, physicist and mathematician Albert Einstein its compound interest.

Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.

Albert Einstein

First, let’s define compound interest. When interest is earned on the principal (basically the balance) that interest is then added to the principal. That new total earns even more interest next period (interest on interest). Then interest is paid on that new amount and repeated. This is true for both interest earning accounts like savings, checking, and money markets as well as investment accounts that earn a return. Both benefit from compounding.

The next part is where we see that this cuts both ways: “he who understands it, earns it; he who doesn’t pays it”. So, you can either be on the receiving end or the paying end of compound interest, and we’re here to tell you that you want to be on the receiving end. Here are some examples that show the benefits of receiving it.

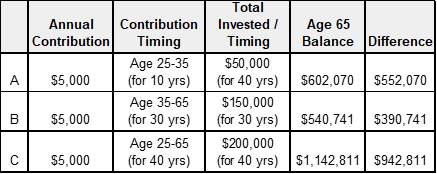

Person A contributes $5,000 a year from age 25 to 35. That’s 10 years of contributions totalling $50,000. It’s invested, and is compounding, from age 25 to 65 (40 years). The balance at age 65, assuming a 7% return, is over $600,000. The last column shows the difference between what was contributed and the ending balance. For person A that is $552,070. They ended up with over half a million dollars more than what they put into it.

Person B contributes $5,000 a year from age 35 to 65; they start 10 years later than person A, but contribute for 30 years instead of 10. That means they contribute a total of $150,000. It is invested from age 35 to 65 (for 30 years). The balance at age 65, still assuming a 7% return, is $540,741. Despite contributing more, person B ends up with less than person A, and “only” $390,741 more than they put into it.

Person C contributes $5,000 a year from age 25 to 65,40 years of contributions for a total of $200,000. Assuming a 7% return invested for those 40 years the balance at age 65 is over $1.1 million. Because of compounding and the 7% return they end up with almost a full million dollars more than they put into it.

Person A invested less but started sooner than person B. Person C started early and kept contributing. So as you can see, the sooner you start saving and investing, the better. Time and compound interest really do matter.

Now, imagine the reverse. Instead of receiving the interest you’re the one paying compound interest on a loan or credit card. It works the same way. For example, say you have a credit card with a balance of $1,000 and you’re charged 20% interest. If you make the monthly minimum payments of $25 it would take you over 5 years to pay off that credit card balance (that’s with no new purchases) and you would pay an additional $661 in interest on top of the $1,000 you spent originally.

You can pay less (possibly much, much less) in interest by paying more than the minimum payment, or better yet, paying your balance in full every month. Like our other example, starting early matters.

We agree with Einstein. Compound interest is the 8th wonder of the world. Just make sure it is working for you and not against you.